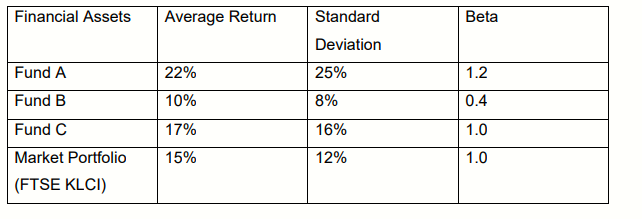

QUESTION 3

Evaluate the three mutual funds using Sharpe and Treynor measure. Given the risk-free rate is 5%.

a) Calculate the following measures for each fund and market portfolio:

i) Sharpe measure

ii) Treynor measure

b) Rank the portfolios using both measures and discuss the differences you find in the ranking.

QUESTION 4

a) You are in a senior management position in a leading international funds management firm. Your Board of Directors required you to analyze FOUR (4) benefits of allocating funds across various countries and geographical regions based on two market dimensions:

i) Developed countries.

ii) Emerging markets.

Answer Preview

Need the complete answer?